Financial Wellness Tips for Medical Expenses

Article by Amber Hollo

Accounting Manager, CU Insurance Solutions

Medical expenses can be extensive and aren’t always easily accessible. Below are several suggestions to help you use your money wisely and still get the care you need. Please note, that you may be able to get additional savings through programs with your health insurer or prescription company.

Ways to Save on Medical Expenses:

- Contribute the maximum allowable to your HSA if you have an HSA compatible plan.

Remember these are pre-tax dollars! More and more items are becoming HSA eligible, including many supplements, OTC medications and supplies.

- Shop lab pricing.

- I found Ulta Lab to be quite a savings for bloodwork

- compairmaine.org is a great tool for comparing lab and medical procedure costs in Maine

- maine.gov/bhr/oeh provides a list of independent lab locations in Maine. A search returns the provider name, site name, address, and county for each option.

- Apply for Care Credit.

They offer multiple years of interest-free payments. I’ll give you my personal example – Lasik eye surgery 2 years ago after a discount for having Anthem insurance: $5000.00. I did not have enough in my HSA to cover the procedure. So, I opened a Care credit account. I put the entire amount on the card and set up payments for 24 months interest-free. I linked that payment to my HSA. I was able to pay the whole amount using HSA pre-tax dollars. As a result, I paid just $5000.00. Say I pay about 20% in taxes. If I had used post-tax dollars from savings/checking, it would really have cost me $6000.00. If I had used a credit card at 25% interest….it would have cost even more.

- Have a savings account for medical expenses.

Ideally, this should have enough to cover a yearly out-of-pocket maximum after HSA total contributions. If you are someone who uses all your HSA yearly, having a savings account for the remainder of your yearly out-of-pocket maximum would mean

no putting medical expenses on your credit card.

- Work with medical practices in establishing payment plans.

If you call their accounting department, many providers can allow/set up a payment plan with you. It’s not usually something advertised, but many do allow it. I’ve done it myself through Firstlight/Mercy and this allows for interest-free payments, either through personal funds or HSA funds as they become available.

- Submit your reimbursements for wellness screenings.

If you have voluntary benefits, they often provide an annual benefit for certain wellness screenings.

Obviously, not everyone has the same circumstances, but the point is, put in a little effort and make your dollars, not you, work harder. I hope you find this helpful!

Should You Offer a DCFSA (Dependent Care Flexible Savings Account) to your Employees?

Article by: Elizabeth Ingram

Vice President of People Strategy, CU Insurance Solutions

A DCFSA is an account that allows employees to pay for childcare (under age 13) expenses pretax. As an employee, although they’ll need to provide invoices or proof of expenses to the DCFSA provider, there are tax savings. Reimbursements cannot be made until after services have been performed, so if the daycare requires payments at the beginning of the week the employee cannot get reimbursed until the end of that week. However, it’s a nice way to keep some extra funds in the employee’s pocket throughout the year, but that doesn’t mean it makes fiscal sense for the employer.

Generally, DCFSAs are administered by third parties (your broker can help you with this if you don’t have a relationship yet) which means there is a cost associated with this benefit. An annual cost is typical, and some third parties have other fees as well. But there are 2 easy ways to determine whether those fees are worth it.

- If you aren’t worried about the expense ($500-$1000/year for a small business) and it makes your employees happy, it may pay for itself in happy, productive employees.

- If you want a hard number comparison, gather your annual costs and take a few minutes to play around in your payroll system. Payroll systems typically allow you to run what I call dummy paychecks through a paycheck calculator. Run 2 calculations on each employee enrolled in the DCFSA; one with their current withdrawal and one without a DCFSA withdrawal. Now, calculate the difference in the employer taxes and multiply it by the number of pay periods per year. If the savings in employer taxes are more than the cost of your DCFSA administration, it’s saving you money. Remember this may change from year to year.

Some benefits you offer may benefit the whole team, while others don’t. But a willingness to consider employee-requested benefits shows you care.

Contact Us

Consumerism – What does that actually mean?

Article by: Pam Huntington

Employee Benefits Specialist – CU Insurance Solutions

In relation to healthcare, it’s defined as, “transforming an employer’s health benefit plan into one that puts economic purchasing power—and decision-making—in the hands of participants”*. It’s about supplying the information and decision support tools you need, along with financial incentives, rewards, and other benefits that encourage personal involvement in altering health and healthcare purchasing behaviors.”* It’s safe to say we’re good consumers when we’re shopping for our next vehicle or the items we put in our carts at the grocery store but are we good consumers when it comes to shopping for our medical procedures and prescriptions? We often go to the medical facility recommended by our providers and grab our prescriptions from the most convenient pharmacy, but is this the most cost-effective? With the increase in health insurance costs and high deductible health plans, now more than ever, we need to shift our mindset around healthcare and begin to take control of how and where we spend our hard-earned dollars.

Check your Carrier portals Register for your carriers’ portals. Not only will you have access to your electronic ID cards, plan, and claim information, but you may also be eligible for additional programs and add-ons. Many carriers offer wellness initiatives with rewards and discounts.

Comparing Bills with Explanation of Benefits It’s important to take the time to compare your provider invoices with the explanation of benefits (EOB) you receive from your insurance carrier. The EOB will show your financial responsibility, which should match the bill you receive from the provider. Don’t just pay without completing this key step. Overpayments can take 60 days or more to be refunded, and if you underpay you may be subject to an unexpected charge down the road.

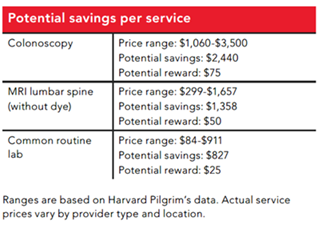

Comparison Tools Most insurance carriers provide cost comparison tools to help you “shop” diagnostic procedures and lab testing. Being a savvy consumer can save you a significant amount of money in your out-of-pocket health insurance expenses. See the below examples from Harvard Pilgrim. Same procedures, but the cost difference can be substantial. Many of these programs offer additional reward incentives for choosing lower-cost facilities. Taking a few minutes to shop for your next procedure or lab test can save you money and put extra cash back in your wallet.

Prescription Resources The convenience of picking up our prescriptions at the same time we grab our groceries seems like a no-brainer, but this might not be the most cost-effective option. Did you know you can “shop” your prescriptions? GoodRx offers a website and mobile app, specifically designed for this purpose. Simply by entering your prescription and zip code information they’ll show you the cost of your prescription at all pharmacies in your area. PLEASE NOTE if you utilize a coupon through GoodRx this will not count towards the deductible/cost-sharing of your medical plan. This is something to consider before using one.

Another tool is to research your drug manufacturers’ websites. Some manufacturers offer coupons as well as financial support. There is a process to apply for financial support, but it can be a momentous financial relief and provide direct assistance towards the deducible/cost-sharing on your medical plan. I’ve personally witnessed the benefits of both these options. I recently had a member whose prescription cost was over $1,000/month through their medical plan and with a coupon, the cost was reduced to roughly $100/month. This is an instance where utilizing a coupon made financial sense.

Essentially you’ve purchased your health insurance. It can be a substantial investment when you consider insurance premiums in addition to the deductible and out-of-pocket expenses. Just like a new vehicle, don’t you want to get the most bang for your buck? Knowledge is power. By just taking a little time you can protect and stretch your dollar.

As always, your Employee Benefits Team is here to assist and answer your questions.

* What Is Consumerism in Healthcare? It’s Lasting Impact On The Industry (nrchealth.com)

Contact Us

What is a Loan Closet?

Article by: Sarah Nash

Training Director, CU Insurance Solutions

I love the saying, “you don’t know what you don’t know.” It has proven to be true in so many areas of my life.

Recently my Dad fell and broke his hip socket. He had to have extensive surgery with plates and pins to repair his hip socket. He had a stay in the hospital followed by a stay in a rehabilitation hospital. I had to learn very fast where to get the equipment he would need when he came home.

His insurance will only pay for one mobility item. Mobility items are wheelchairs, walkers, crutches, shower chairs, portable commodes, or a toilet seat riser. In my Dad’s case, his insurance paid for him to have a walker. Dad’s Physical Therapist asked him if he’d received all the equipment he would need at home. Previously the Case Worker had told my Dad and us that she’d take care of all that. It turns out that the Case Worker does not arrange for your mobility items for use at home. You need to make those arrangements!

The wheelchair, crutches, shower chair, commode, and toilet seat riser were now my mission. Where to find these items, if I had to buy them all, or if we knew anyone that we could borrow these items from. In true Murphy’s Law fashion, I had three days to procure all items.

As I started searching, I first looked at Amazon.com. A basic wheelchair is $110. A basic walker is $30. Basic crutches are $25. A shower chair that sits outside and inside the tub is $55. A toilet seat riser is $27. A bedside commode is $33. So far, we are at $280 for the most basic versions of these items. That number might not sound like a lot of money to some. If you are out of work, do not have disability income, or are already on a fixed income, $280 can be an overwhelming amount to spend for these items that you may never use again once you are recovered.

The Physical Therapist gave my Dad a two-page document titled Loan Closets. Talk about a total game changer?! I had no idea that these places existed and as I tell others about the Loan Closets, it’s been proven to me that not a whole lot of folks know about these resourceful places. I will attach the list for reference. First, I’ll tell you a bit about them.

The Loan Closets are places where you borrow (mostly) FOR FREE, (there is one place on my list that charges a small fee), the mobility items you or your loved one needs to recover. Not all are equal in that some will have only basic items, but others have most all mobility items you may need, even hospital beds. Some are limited to residents of that town only, but others will lend to anyone from anywhere in Maine. We used the one in Standish which will loan to anyone whether they are a town resident or not. They are located at the Kiwanis Club on Route 25. If you’ve ever been to Kiwanis Beach, you can easily find this place. They have a garage filled with mobility items. These locations are typically run by wonderful volunteers. You might have to call and make an appointment to go and get the items you need. Be sure to bring a tape measure and your notes.

Here is a List of Maine Loan Closets

Now that you know these wonderful places exist, let me share my newfound knowledge about some mobility items.

Wheelchairs

There is not just one type of wheelchair. There is what is called a transfer wheelchair. This is to be pushed from behind by someone other than the person in the chair. This type will have no handgrip rail on the wheel of the chair for the occupant to self-propel the chair. Of course, this is the first one I brought home only to find out I had the wrong kind. It never dawned on me to look and see if the handgrip rail was there. I thought all wheelchairs had that on them. I learned my lesson and had to go back and swap it out for the correct kind of chair. Did you know that some wheelchair tires take air just like your car tires? I did not know this. I also did not know that the air compressor chuck we use for our car tires will not fit on the wheelchair valve stem. Any guesses how I figured this out? Let’s just say the hard way, outside in freezing weather. You will need an air compressor chuck that will fit bicycles and other types of similar items. Other wheelchairs have solid wheels, and no air is required. Now I know. Had I known prior, I might have looked for solid wheels, to avoid said air compressor/valve stem issues.

Crutches

Not all crutches are the same size. Be sure to factor the person’s height in when choosing crutches. They should not fit tight up to your armpit. There should be space between your armpit and the cushion on the crutch.

Toilet Seat Risers

Toilet seat risers are not all equal. The one I brought home for my Dad sat on the toilet seat and had no handles. He did say it was like sitting on cold concrete. Luckily, he could get by without that item. They also make toilet risers with handles that sit over the actual toilet almost like a chair. Make sure you measure your area where your toilet is positioned in your bathroom to be sure it will even fit in the spot. This goes along with the adage, “measure twice, cut once”, or if you are me, measure twice, and measure a third time to be safe.

Walkers

Walkers have hard wheels and make A LOT of noise on tile floors. You can upgrade the wheels to some softer, more quiet wheels should you have downstairs neighbors. Tennis balls are put on the rear stationary walker legs to help them slide on the floor. Carpeting, area rugs, and throw rugs will not be your friends during this time.

Shower Chairs

Shower chairs also proved to have more than one model. There are chairs that sit inside the tub. Some have a back and armrests. Some do not. There are “double-wide” chairs so that one side sits in the tub and the other side sits outside the tub. One can sit on the seat outside the tub and shimmy over to the other half that is inside the tub. This is safer for some than stepping over the side of the tub to get to the chair inside the tub.

Vehicles

The last bit of helpful information has nothing to do with the Loan Closets, but it was another thing I had never considered. If you were injured and suffered a mobility issue would you be able to get in and out of your current vehicle? My Dad drives a Toyota Tundra and my Step-Mom drives a Jeep Wrangler. Dad’s injury prevents him from getting up/in both of those vehicles due to their height off the ground.

Hopefully this information is helpful and informative to anyone who suffers an injury or is left caring for someone with a mobility issue. As I was researching how to get the Loan Closet list from New England Rehabilitation Hospital in Portland Maine, my phone call was directed to Maine Medical Center. The nice woman who answered was named Martha. When I told her what I was trying to find, she had never heard of this “list” and asked if I could fax it to her. She gets many calls asking where folks can get mobility items. The only place she knew to refer them was to Black Bear Medical. I looked on their website and it doesn’t list prices, so I cannot speak for the cost to purchase any items from them. (Black Bear Medical is for purchasing items, and the cost is often offset by insurance.) Please note the information on the attached list is subject to change and accurate as of March 2021.

Please note that most of these Loan Closets will accept donations of mobility items you may have and not need. They do ask that you make an appointment to drop off any donated items rather than leaving it unattended.

What is a MEWA?

Article by: Elizabeth Ingram

Vice President of People Strategy, CU Insurance Solutions

MEWA is an acronym for Multiple Employer Welfare Association. It’s a group of employers with some sort of commonality that joins together, primarily for the purpose of offering employee benefits.

Here in Maine, many Credit Unions and Credit Union Service Organizations (CUSOs) are part of a MEWA named the Maine Credit Union League CU Insurance Solutions (MCULIT) that offers medical insurance. However, a MEWA can offer other benefits (dental, vision, etc. as well). The idea is that working together can provide cost savings or better benefits for employers and their employees.

MEWAs have to be approved by the state Bureau of Insurance (BOI) since they operate a bit like insurance companies. However, a MEWA generally works with an insurance company to either run the health insurance plan completely (a fully-funded plan) or provide a network of providers, negotiate discounts, and provide stop-loss insurance (a self-funded plan). MCULIT is a self-funded plan which works with Anthem.

If you are a Maine Credit Union or CUSO who isn’t already part of our MEWA, MCULIT, and you’re interested in learning more, please reach out to our Employee Benefits Specialist, Pam Huntington at phuntington@insurancetrust.us or 207-641-5410.

What You Need to Know About Early Retirement Executive Compensation Packages and Health Insurance Coverage

Article by: Kim Daigle

President/CEO – CU Insurance Solutions

Does your credit union currently offer an early retirement executive compensation package that includes health insurance coverage?

You need to be aware that just because you were offered an early retirement package by your credit union’s Board of Directors does not mean that it is necessarily compliant with the organization’s current or future health insurance companies’ provision for retired employees.

Over the last 3 years, I’ve discovered that many credit unions’ executive compensation plans do not align with the insurance companies’ policies. To qualify for your employers’ health insurance coverage, you must be working the minimum number of hours to remain on the active group plan. This will vary but minimum hours are dictated by each carrier and your plan documents and must be consistent for all employees.

If you plan to retire before age 65 and have an executive compensation package from your Board of Directors that includes health insurance coverage, you NEED to ask the following questions:

- Does your current or future health insurance company offer retiree coverage for those retiring under age 65?

- Just because your employer keeps you on the active group plan doesn’t mean you are eligible for coverage. If your credit union keeps you on the active group plan and your current or future health insurance does not allow retired employees under age 65 on the active group health insurance plan, you’re not eligible for coverage.

- If your health insurance carrier does allow under age 65 retirees to stay on the active group health insurance plan, make sure you get this in writing from your health insurance carrier including the parameters in which they allow an under age 65 retiree to be on the current plan.

- If your health insurance plan does not allow you to be on the active group health insurance plan under 65, here are the options you have:

- If your credit union is large enough to be COBRA eligible (20+ FTE or in a MEWA), this would allow for coverage for 18 months from your retirement and end date on the active plan.

- If COBRA will expire prior to turning age 65, you can then enroll in an individual marketplace health insurance plan through healthcare.gov until you become eligible to enroll in Medicare. These plans are offered on the “exchange” but can be quite costly since it based off your current age.

- If your credit union is not large enough to be COBRA eligible, you can enroll in the individual marketplace health insurance through healthcare.gov.

- Your employer CAN contribute to the cost of your COBRA coverage AND/OR your individual marketplace health plan coverage.

CU Insurance Solutions uniquely understands credit unions and Employee Benefits. Please utilize our agency as a resource to help make sure your executive compensation package is compliant.

Contact Us

Finding Hope and Balance as a Parent in “The New Normal”

Article by: Heather Baird

Account Manager – Employee Benefits

This is for the other working mamas, dads, and caregivers out there.

Going into 2020 none of us could have foreseen the changes our lives have endured over the last year. The terms of the year have included “unprecedented times” and “our new normal”. There has been nothing “normal” about this year! As a working mom of three small children, this year has been a roller coaster of ups and downs, and if I’m going to be honest, there have been a lot of down days. I would say we’re surviving our new normal rather than conquering it most days. Early in the pandemic, I saw this quote: “In the rush to return back to normal, use this time to consider which parts of normal are worth rushing back to” (Dave Hollis). Meditate on that for a minute.

As women (kudos to you men as well), many of us are inherently givers. We take care of our people, spouses, children, family, neighbors, friends. We do this to a fault, and sometimes to the detriment of our own health and well-being. By the end of many days, I find there is not enough energy left for me. Self-care? What’s that, and more importantly what does it look like for me? After my third child was born, I finally took time for myself and began seeing a therapist. I remember she looked at me and asked, “Do you think you’re depressed?” I remember pausing a minute and saying, “Probably, but I don’t have time to be depressed!”

Looking back, I laugh. It’s so true. How many of you are tired? Our culture has become so goal-oriented and driven we’ve lost sight of balance and rest. It’s become a badge of honor to be overworked and exhausted. We work long hours at our day job and then jump right into our other roles at home. It’s a whirlwind of go, go, go, and turning around and doing it again the next day.

As a child of the ’80s, I remember the days when it was a big deal to rent a movie at Blockbuster on Saturday night realizing you would get an extra day free. That’s right; businesses were closed on Sundays. What a novel idea, a day of rest. What if we went back to that concept and allowed ourselves time each week to truly rest? To forget about the laundry and dishes and instead enjoy a good book, pick up a hobby, or spend quality time with our loved ones.

I’ve heard people say that an addict needs to hit rock bottom before they come to a place where they can start their journey towards healing. This year has brought me to my knees on more than one occasion, and I’m realizing that sometimes it’s not until we’re in our darkest moments that we finally start to see the light. The light was always there, we were just too busy and distracted to see it.

As hard as this year has been it’s been extremely enlightening. “They” say in every storm there is a blessing. I’ve finally come to a place of realization that I need healthy boundaries and structured balance in my life, and I’m finally taking the time to figure out what self-care looks like for me. It’s my heart’s hope each of you take the time this pandemic has given us to reflect on your lives too. Don’t go back to “normal.” You deserve better than normal!

Most importantly, know you are not alone. There is nothing normal about this. It’s chaotic and stressful, but we’re all in this together. It just looks and feels different for each of us. That mom down the street or on social media may look like she has it all together, but I guarantee she struggles too. If you’re struggling and don’t know where to start check-in with your HR contact, benefits administrator, or primary care physician to see what resources are available. As dark as your days may seem there is hope.

And for that mama in the drop off lane whose kid is having a meltdown or hasn’t showered in two days, this is for you, “I respect parents who have it all together, but parents who stumble in to drop their kids off at school, looking like they just got attacked by a flock of angry birds? Those are my people!” (author unknown)

Mental Health | United Way 211

What is My Emergency Fund?

Article by: Elizabeth Ingram

Vice President of People Strategy, CU Insurance Solutions

For me, this year’s pandemic reminded me of the importance of an emergency fund. I know that there are scads of suggestions of how much to save and how because I’ve read them. I also know that storing 3 to 6 or even 12 months of savings in an easily (but not too easily) accessed account is not practical with childcare costs, debt repayments, and just life. I direct a portion of my income into savings each pay period, but honestly, that savings isn’t just for emergencies, it’s for home maintenance and sometimes presents even as we seek to grow it. Knowing that we didn’t have the suggested emergency savings in the midst of a pandemic freaked me out.

But just last month I realized something; in my worst-case scenario where both my husband & I lost our jobs, we wouldn’t just use an emergency savings account, we’d use everything to take care of our family. I realize that there are many other worst-case scenarios out there, but I cross my fingers and pray that insurance covers most of them; I know it won’t pay the bills if our jobs are gone.

If our jobs were gone, we wouldn’t be paying for childcare thus cutting our biggest expense from our budget. We would be paying a lot more for insurance, thus increasing our budget anyway. But we wouldn’t just use our savings account, we could use the money in our HSA account for the COBRA expenses. We could apply for unemployment benefits. If we absolutely had to, we could pull money from our investment account, the contributions previously made to my Roth IRA, the cash value from our whole life insurance. None of these options are ideal but knowing that there is a little more money available in case of my worst-case helps me sleep at night.

In an emergency, all of your money is an emergency fund. So, figure out where that money is and give yourself a little grace if what you have isn’t as much as you think it should be. I know you’re trying.

A Car Accident with Kiddos – Safety, Health & Car Seat Replacement Info

Article by: Elizabeth Ingram

Vice President of People Strategy, CU Insurance Solutions

Now, I sincerely hope that you are never in the position that this information is of any use to you. But let’s talk about car crashes. Last year, my husband’s SUV was hit on an icy highway; it flipped and the car was totaled; thankfully, his only injury was a bump on the head. Last week, my car got rear-ended as I waited to turn at a four-way intersection. There was minor damage to the cars and no injuries, but my not-quite two-year-old daughter was in the car, so I called the pediatrician. So, here’s the skinny…

At the Scene of the Accident

- Pull over to a safe spot with the other vehicle if possible

- Call the police

- Exchange license, insurance, and registration information

- Take pictures of the damage

- After speaking with the police, you can head out

After the Accident

Be sure to call your insurance carrier ASAP to file a claim; this can sometimes be done via app or online as well.

If you are feeling the effects of the accident, you should also call your doctor.

If you had kids in the car, you may choose to call the pediatrician even if they seem to be fine especially if they might not have the words to tell you if they don’t feel well. My pediatrician let me know under what circumstances I should call back. They also let me know that their car seat specialists suggested I call the car seat manufacturers.

Replacing Your Car Seat/s

The NHTSA site (Car Seat Use After a Crash | NHTSA) states that car seats need to be replaced after moderate to severe crashes even if they weren’t in use at the time of the accident. However, when I checked with my car seat manufacturer (it happens to be Graco), they stated I should replace the car seats after ANY accident. Think of it like a bike helmet after you hit your head; it needs to be replaced even if there isn’t any visible damage because the structural integrity may be compromised. I know this can seem crazy expensive.

Next, you need to reach out to your insurance carrier and find out what they need to reimburse you for the cost of replacing the car seats. When my husband’s car was totaled, I just needed to provide a receipt, but this time we need to provide a picture of the old car seats (with the straps cut), receipts, and pictures of the new car seats. It’s a little bit of a process, but the reimbursement (if you’ve hit your deductible) definitely makes it worth it.

Stay Safe!

What can a credit union do for you?

Article by: Sarah Nash

Account Relationship Manager – Member Lending Division

There’s a great saying: “You don’t know what you don’t know.” This rings true in so many areas of life. Unless you have experienced something yourself or have learned from a family member or friend; you just are not aware of some of the things out there! I’m going to use credit unions as an example.

Credit unions have been in North America since 1901. Alphonse Desjardins is credited with bringing credit unions to Levis, Quebec. This credit union was in his home! LaCaisse Populaire de Levis (The People’s Bank of Levis) was its name. The first deposit was 10 cents. On April 6, 1909, St. Mary’s Cooperative Credit Association, the first U.S. credit union opened in Manchester, New Hampshire with assistance from Alphonse Desjardins. There is a wonderful account of all the historical data regarding credit unions that the NCUA-National Credit Union Administration has put together on their website. I’ll leave you to read all the history if you choose. Historical Timeline | National Credit Union Administration (ncua.gov)

Maine has about 54 different credit unions. The word “about” is used in that statement as there are a few that are currently merging with other credit unions. The largest credit union in Maine is Atlantic Regional Federal Credit Union. They have $816.93 million in total assets and over 48,246 members. There’s a list of all the Maine credit unions shown here: Maine Credit Unions (ncuso.org) There’s a decent likelihood that a credit union is close to where you work or live. I urge you to visit (call ahead due to Covid-19 restrictions) one and see what they have to offer.

Most likely you have used a bank. Most banks are for-profit, meaning they make money on your money. Credit unions are not-for-profit because their purpose is to serve their members rather than maximize profits. Credit unions are owned by their members. Credit unions are understood to be better than banks because banks tend to have higher overhead costs, which are passed on to you, the customer. Credit unions pass on their lower overhead costs to their members (customers) in the form of higher deposit interest rates. You can find rate and fee schedules online to compare how a credit union benefits their members. I’ve attached one here for reference. This is for Lincoln Maine FCU. This is just one example. Rate-and-Fee-Schedule.pdf (lincolnmainefcu.com)

Most people know that a credit union can offer you savings accounts and checking accounts as well as loans. Most don’t know all the other amazing things credit unions can do for them. I feel as though the information on what they do offer needs to be shouted from the rooftops! There is a large percentage of our communities that are not aware of what a valuable resource a credit union can be for them!

Let me give you a list of the things a CU can do for you. I’m going to use Lincoln Maine FCU as an example. Not all CUs have all the same programs, but this will give you a better idea of what most can do for you! Look at the different accounts offered*.

- Checking/Savings also referred to as Share Draft/Share Accounts

- Club Accounts

- Educational Share Accounts

- Free4ME Checking

- Health Savings Account

- IRAs

- Kasasa

- Money Markets

- Share Certificates

- Youth Accounts

Let’s talk about loans*! Yes, auto and home loans are included. Did you know that not all credit unions base their lending on just your credit score? They use many more factors in their lending practices. Do you know about these other kinds of loans?

- Christmas Loans

- Commercial Loans

- Consumer Loans

- Fuel Loans

- Personal Loans

- Real Estate Loans

- Vacation Loans

- Wedding Loans

- Visa Credit Cards, what? Yes, you can get a CC from your CU!!

It’s helpful to know that when you have certain loans with the CU, there are programs* you can enroll in to help keep you in a great financial position in the event of death, disability, and job loss. There are also programs that can keep you in a great financial position if you were to have a car accident or total your vehicle. Ask the CU you visit about these products. There are programs such as Debt Protection, Credit Life and Disability, Mortgage Life and Disability, Guaranteed Asset Protection, Auto Deductible Reimbursement, and Total Restart. There is even a vehicle service program you can purchase with your auto loan that can fix your car if it breaks down. Some credit unions even offer pet insurance!

OK, now let’s touch on Membership Benefit Options! Did you know that as a CU member you are eligible for special group discounts for several products and services*? Here are some packages offered by Lincoln Maine FCU.

- Life Insurance

- Auto/Home Insurance

- AD&D (Accidental Death and Dismemberment)

- Debt Protection

- MDLive Health Insurance

- Financial Planning

Your local credit union can do all of what I have listed above AND THEN SOME! They offer credit counseling and financial fitness education, and they genuinely care about your financial well-being. You are more likely to get help from your credit union on things that aren’t even related to the credit union. This is because they imbed themselves in their communities. I’d be willing to bet that your local credit union could point you in the right direction for whatever you needed. If you need a lead on a physician, carpenter, mechanic, church, entertainment, charities, or any other local resource, there’s someone at that local credit union that can assist you by referring you to someone who can help. I like to think of credit unions as extensions of your family. The care and concern they exhibit while helping their members succeed is real. They do not treat people like a number. They will likely get to know you on a more personal level, and you’ll end up on a first-name basis with the team members in your local credit union. I urge everyone to find a local credit union and get to know what they can do for you. I believe you will be impressed with the service you receive no matter which one you choose. I would suggest using the internet to find a local credit union and visit their websites to see if they carry the program you might be interested in for your financial well-being.

*Please note that Lincoln Maine FCU was used as an example only. They may not have all packages/programs, loans, products/services listed in this article, nor will all the other Maine credit unions. Each credit union is unique and offers different packages/programs, loans, products/services to their members.